Weighing up Crop Hail Insurance versus Multi-Peril? Kansas weather is unpredictable – making the security of crop insurance coverage a near-necessity for many producers. More than 80 years after the creation of the Federal Crop Insurance Program, farmers can access two types of coverage: Multi-Peril Crop Insurance (MPCI) and Crop Hail Insurance.

Choosing the right type of coverage for your operation goes beyond consideration of extreme weather. Crop Hail Insurance and MPCI differ in many ways from program structure, to coverage timelines, to protections offered.

Ready to explore which type is right for you?

Key Takeaways

What Is Multi-Peril Crop Insurance (MPCI) and What Does It Cover?

Multi-Peril Crop Insurance is a government-subsidized policy, offered as part of the Federal Crop Insurance Program. Established in 1938 with the passing of the Federal Crop Insurance Act, the program looks to provide affordable crop insurance to farmers. This helps to maintain the viability of farming and ensure the stability of the nation’s food supply.

MPCI coverage does just that by covering the loss of crops due to:

What Is Crop Hail Insurance and What Does It Cover?

Crop Hail Insurance is a privately provided policy that offers protection against crop losses not insured under MPCI. In a region where hail can be a prevalent threat to farmers and their yields, Crop Hail Insurance secures against losses caused by:

Both Crop Hail Insurance and MPCI provide needed protection to Kansas farmers against circumstances outside their control. However, three key differences create unique applications for each.

Difference #1: Crop Hail Insurance Prices Vary Between Insurers

Because Crop Hail Insurance is offered by private providers, policy prices are set by the individual insurance companies.

Conversely, MPCI is provided through a public-private partnership between the federal government and 15 private insurers approved by the United States Department of Agriculture Risk Management Agency (USDA RMA). The RMA establishes industry-wide premium rates for all insurable crops at one price. All prices are the same throughout the program.

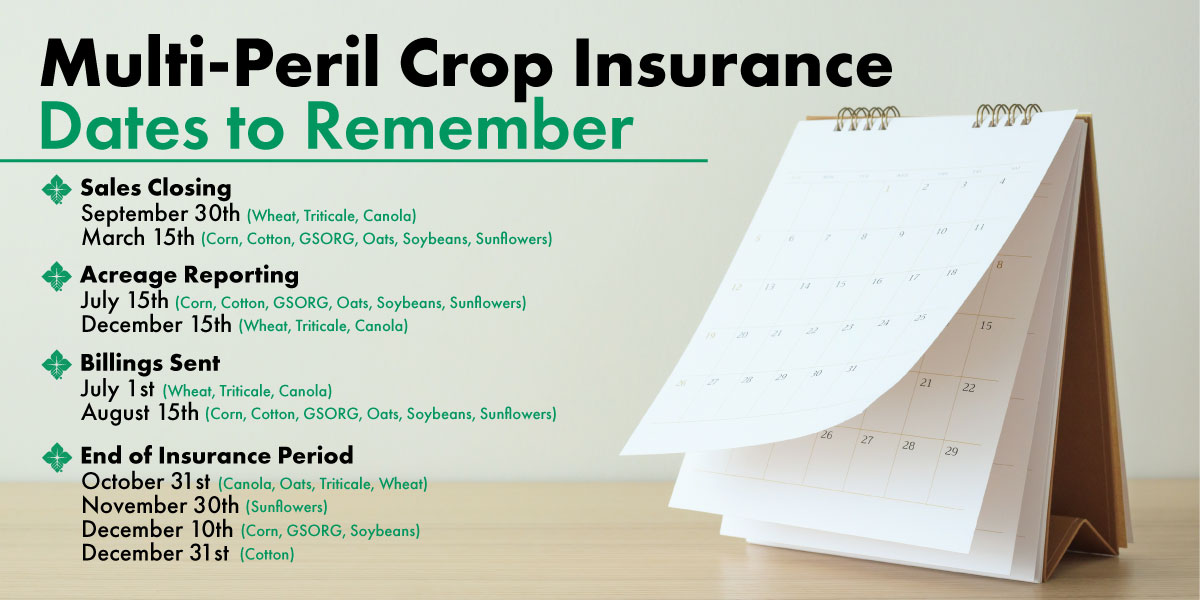

Difference #2: Multi-Peril Crop Insurance Has a Coverage Deadline

Farmers looking to purchase MPCI must do so before planting and prior to the March 15th coverage deadline.

However, Crop Hail Insurance offers greater flexibility by allowing producers to purchase coverage at any point in the growing season.

Difference #3: Crop Hail Insurance Offers Additional Security

While MPCI provides affordable coverage to help farmers secure their livelihoods, Crop Hail Insurance serves as an added layer of protection.

In fact, it is often used to protect against crop losses that are not insured under the federal program or fall below their MPCI threshold.

The nature of hail-producing storms may leave certain portions of a crop unharmed while others are damaged. Crop Hail Insurance can supplement MPCI as additional protection in the event that a claim is less than the deductible for Multi-Peril Crop Insurance.

The security offered by Crop Hail protection also extends beyond the name to insure against losses from fire, lightning, wind, and damage occurring during transit, making it an attractive option for farmers looking to protect high yield crops.

Multi-Peril Crop Insurance vs. Crop Hail Insurance

| Multi-Peril Crop Insurance | Crop Hail Insurance | |

|---|---|---|

| Protects against losses in crop yields… | Yes | Yes |

| Is government subsidized… | Yes | No (privately provided) |

| Offers additional coverage for high yield crops… | No | Yes |

| Can be purchased… | Before sales closing date | At any point in the year |

| Cost of coverage is… | Determined by the RMA | Set by private agencies |

Are There Other Types of Coverage Available Through High Plains Farm Credit?

Yes! High Plains Farm Credit is proud to offer a comprehensive range of crop insurance policies that include both yield protection and revenue protection. Additional types of insurance policies include:

Which Coverage Is Right for You?

The High Plains Farm Credit team is ready to help you customize a crop insurance plan designed to meet the needs of your unique operation. We know the ins-and-outs and can help you determine the right mix of coverage when choosing between Crop Hail Insurance and Multi-Peril Crop Insurance.

Contact us today to explore the options and get protected!

Equal Housing Lender

Equal Housing Lender