With cattle prices reaching historic highs, producers have more at stake than ever. That means protecting your margin is no longer optional – it’s essential.

Livestock Risk Protection (LRP) is a federally subsidized insurance program designed to help cattle producers guard against falling market prices while still benefiting from rising markets. In this article, you’ll learn how LRP insurance works, how to customize coverage, and how it can increase profitability for your cattle operation.

Key Takeaways

What is Livestock Risk Protection (LRP)?

Livestock Risk Protection (LRP) is a price risk management tool administered by the USDA’s Risk Management Agency (RMA).

It protects livestock producers from market price declines caused by:

Unlike traditional insurance, LRP does not cover:

Instead, it guarantees a minimum price floor for your cattle.

How LRP Works (Simple Breakdown)

LRP allows you to lock in a minimum price for your livestock while keeping upside potential.

Here’s how it works:

- 1

Choose your coverage details (weight, price, timeline).

- 2

Calculate a subsidized premium.

- 3

If market prices fall below your selected price, you receive an indemnity payment.

- 4

If prices rise, you sell at the higher market price.

Note that your LRP premium is not due up front when coverage is purchased. You pay the premium when you sell cattle at the end of the endorsement.

This creates a safety net without limiting profits.

LRP coverage doesn’t protect against mortality, condemnation, physical damage, or disease.

Instead, it allows livestock producers to maximize profits on the sale of livestock by allowing them to wait to market until cattle and swine reach a target weight and by providing payments if regional and national cash price indexes fall below a floor price.

This market protection is more important than ever in today’s environment. With more dollars at risk, LRP can protect a portion of your money that’s on the line. LRP provides an added layer of security when it doesn’t take much for external factors to trigger a price drop in the market.

How to Customize LRP to Your Operation’s Needs

One of the core benefits of Livestock Risk Protection is the ability to customize it to your cattle operation’s needs and your specific plans to market livestock.

Eligible Livestock

LRP coverage allows you to insure:

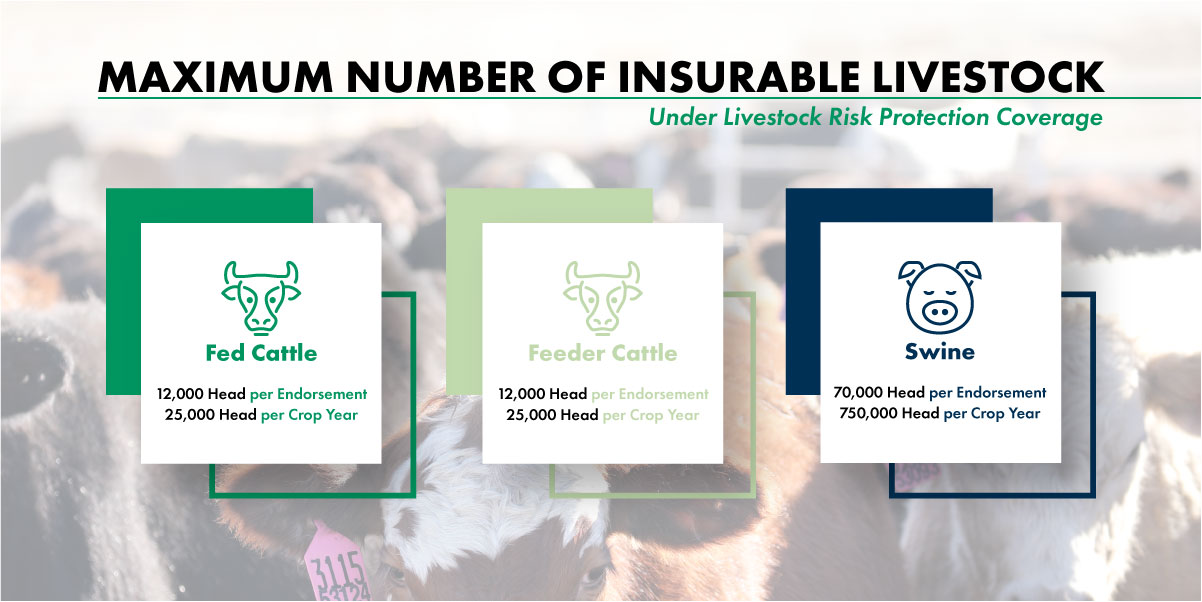

The RMA allows up to 12,000 head per endorsement and 25,000 head per crop year for fed or feeder cattle. Producers can ensure up to 70,000 head of swine per endorsement and 750,000 head per crop year.

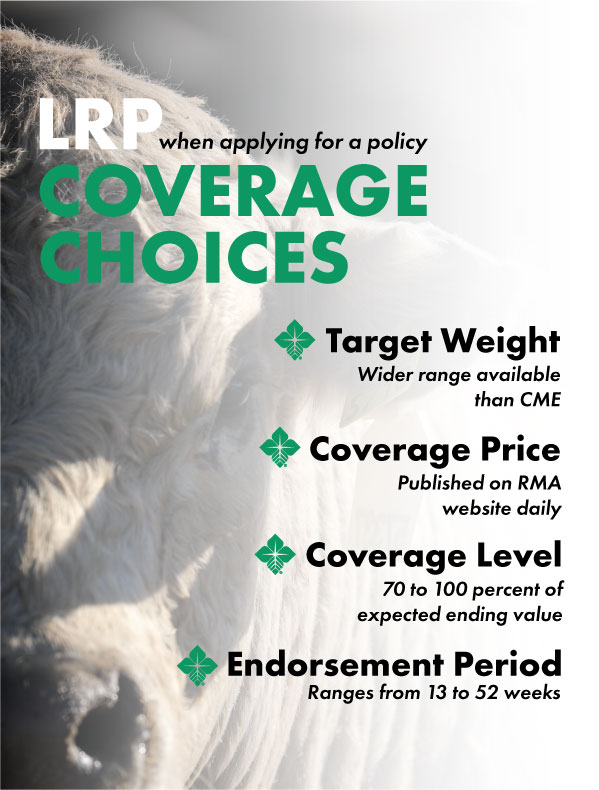

Choices When Applying for Coverage

In addition to options provided for type of livestock, you can tailor your policy by selecting:

When applying for LRP, you’ll select a target weight based on a range that’s wider than the Chicago Mercantile Exchange. This target weight is defined differently for cattle and swine. Feeder cattle are paid based on live weight while swine are paid on lean weight.

You application will also consist of choosing a coverage price and coverage level ranging from 70% to 100% of an expected ending value.

You’ll also set a coverage endorsement period ranging from 13 to 52 weeks.

The closer your endorsement period matches your sale date, the more accurate your protection.

LRP Premium Costs Explained

LRP premium depends on:

The USDA subsidizes 20%-35% of premiums, significantly lowering cost. These premiums are subsidized as part of the federal crop insurance program, covering a portion of the producer premium and helping producers lock in price protection.

Example: LRP Cost Calculation

Let’s break it down with a real-world example.

A producer is looking to insure 100 head of feeder steers cattle. The target weight to market cattle is 7.00 cwt each. The producer has a 100% insured share in the cattle. With a 100% coverage level at a one- week endorsement, a coverage price of $361.31, rate for coverage price of 0.04438, and a premium subsidy of 35%, the cost of LRP coverage can be calculated as follows:

- Number of livestock: 100 head of feeder steers cattle

- Target weight to market cattle: 7.00 cwt each

- Insured share: 100%

- Coverage level: 100% at 13-week endorsement

- Coverage price as a percent of the RMA’s expected ending price: $361.31

- Rate for coverage price: 0.04438

- Premium subsidy: 35%

Calculation Summary:

100 head * 7.00 cwt = 700.00 cwt

700.00 ctw * $361.31 (coverage price) = $252,917 total liability

$252,917 total liability * insured share (1.00) = $252,917 insured value

$252,917 total liability * 0.04438 = $11,224 total premium without subsidy

$11,224 *35% = $3,928 (35% subsidy)

$11,224 – $3,928 = $7,296 producer premium

Guarantee per head: $2,529.17

Cost per head: $72.96

*This shows how affordable price protection can be at scale.

How to Document a Loss With LRP

At the end of that endorsement period, if the market price falls below the established coverage price, you may receive an indemnity payment to cover the difference. This protection from profit loss is one of the central benefits of LRP insurance coverage. However, producers also benefit from price increases without penalty.

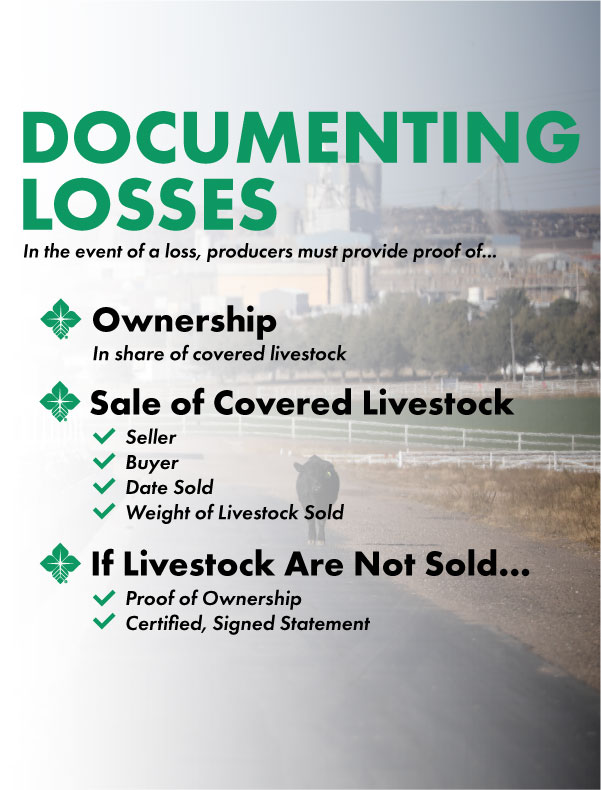

Documentation Requirements for Claims

In the event of a loss, required documentation must verify:

If you do not sell feeder cattle at the end of the period but a loss occurs, you must provide proof of ownership and a certified, signed statement, attesting that covered livestock were not sold before the end date but were marketable at that time.

Note that you must sell cattle covered by fat policies at the end of the endorsement.

Example: LRP Loss and Indemnity Calculation

Running the numbers on a potential indemnity can help you decide if LRP makes sense for your cattle operation. Let’s continue the example from above.

The actual price is the actual ending value the day your endorsement concludes. In this example, the actual ending value is $358.00, which is less than the coverage price selected ($361.31). Based on this information, you can calculate the LRP indemnity as follows:

100 head * 700 cwt target weight * ($361.31 – $358.00) * 1.00 share = $2,317 indemnity

Recent Updates to the LRP Program

Since 2002, Livestock Risk Protection insurance has offered flexibility and security to cattle producers subject to the markets and ever-changing external factors. Program updates in 2022 offered additional advantages to ranchers.

LRP Coverage for Unborn Calves and Swine

Under the update, unborn calves and swine can be insured with LRP. The RMA defines unborn feeder cattle as livestock not born on the coverage effective date that are expected to be marketed before the end date.

Livestock must be born prior to the end date and the number of cows must be able to produce the number of unborn calves. Cow-calf producers should have ownership of the pregnant cows, as established by the following examples of documentation:

Unborn swine have special documentation requirements in the instance of a loss. When documenting the sale, the insured may not be the seller but might be the buyer instead.

Increases to Maximum Number of Insurable Livestock

The update to LRP coverage for cattle allows for up to 12,000 head per endorsement and 25,000 head per crop year for fed and feeder cattle. Producers can now purchase coverage for up to 70,000 head of swine per endorsement and up to 750,000 per crop year.

Your cattle operation is your passion, your livelihood, and your life. And while you can’t control the weather turns, demand drops, and increased input costs that and shift the market, you can put some security back into how you run your ranch.

When uncertainty brings stress, LRP gives you more control over when you market and what you profit.

Frequently Asked Questions

What Does LRP Insurance Cover?

LRP covers price declines – not death, loss or disease.

When Do You Pay LRP Premiums?

Premiums are due at the end of the coverage period.

Can You Still Profit if Prices Rise?

Yes. LRP does not cap your upside.

Who Qualifies for LRP?

Any eligible livestock producer working with an approved agent qualifies for Livestock Risk Protection.

Equal Housing Lender

Equal Housing Lender